What Are the Real Threats to the Economy?

Is the sky falling? Are we all doomed? Are we on the cusp of stagflation or hyper-inflation? Is this the beginning of the worst recession since the 1930s? The short answer is no.

Is the sky falling? Are we all doomed? Are we on the cusp of stagflation or hyper-inflation? Is this the beginning of the worst recession since the 1930s? The short answer is no.

Chris Kuehl, PhD, managing director of Armada and economic analyst at Industrial Heating Equipment Association, explains why the future may not be all doom and gloom. Read on to discover a positive outlook on the economy in this original content piece, originally published in the June 2022 Heat Treat Buyers Guide print edition.

Managing Director, Armada, Economic Analyst, IHEA

The frothy coverage of the economy has been an exercise in extremes and one has to wonder why. Especially when we look at the actual data. The signals that are being sent are not all that dire. This is not to say that there are no problems to be aware of and there are most definitely some impending threats, but the near hysteria that shows up almost hourly is not justified by the facts — at least not as they are emerging right now. Why do some economists present these extremely pessimistic assessments and assert that a major catastrophe lies ahead?

The truth is that economists are not all that good at forecasting and predicting despite the fact this is supposed to be our job. The reality is that we have predicted 13 of the last three recessions. The comparisons between an economist and a meteorologist are not flattering but both professions have the same challenge. The data changes and it changes fast. The real purpose of the dire economic forecast is to warn. It is essentially pointing out that the economy is headed for a brick wall unless something changes. The prediction of a major recession in 2030 or 2035 or 2050 is nothing more than a call to action. If the issues that are affecting the economy are not dealt with, the likely outcome will indeed be the recession or other economic calamity that has been forecasted.

The predictions of doom and gloom are designed to call attention to major issues that demand attention sooner rather than later. All are driving the negative performance of the current economy. None of these will be easy to deal with and failure to either prepare for the impact or find a way to avert the disaster will indeed mean the economy could be headed for strains that will significantly hamper growth.

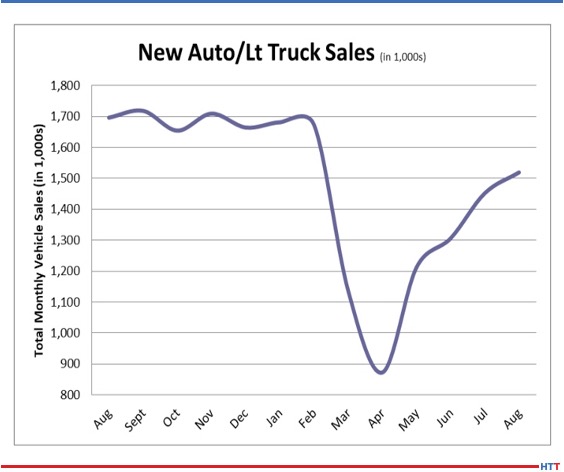

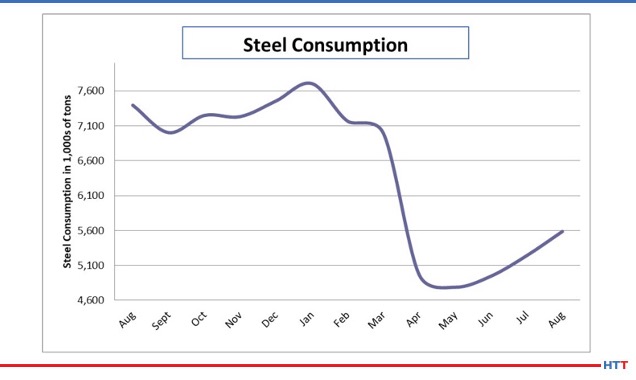

At the top of the list is the supply chain. It is safe to assume that the old system will never return. The breakdown in globalization has been due to everything from geopolitical tension to the desire on the part of companies to have better control of their processes. It is estimated that there will be a trillion dollars of reshoring in the U.S. this year alone. Nearly 70% of those doing business in China want to shift significant production to the U.S. or at least to North America. Robotics and technology allow companies in the U.S. and Europe to compete with those low production cost platforms in other countries. Despite these moves, China and other nations provide trillions of dollars of goods to the U.S. and the rest of the world which means that the reshoring effort will not eliminate the importation of material from China and elsewhere, but the dependence that has developed on the Chinese export sector will diminish. Along with the effort to bring production back to the U.S., there will be diversification when it comes to these overseas sources. There will be expansion to other Asian states such as Vietnam, Thailand, and Malaysia and there will be efforts to expand to more Latin markets such as Colombia and Brazil. Even states in Africa such as Nigeria, South Africa, Ghana, and Kenya will see efforts to expand. It is important to note that all these nations provide opportunities but also challenges.

The next challenge is connected to both the labor issue and the supply chain. Companies that struggle to find the people they want to hire will turn increasingly to automation and robotics. This has already occurred in the manufacturing sector as machines have largely replaced the people who once worked on the line in the factories. Now the automation revolution has reached the service sector with developments such as online buying, self-serve retail, and complete conversion to consumer driven interactions. The need for the labor that once dominated the service sector has largely diminished. The technology demands a higher-level worker, and those people are in even shorter supply than other skilled workers. The future is one of cobots — people interacting with and working alongside machines that have the ability to do their own problem solving. It is the robot and technology revolution that has spurred so much of the reshoring effort as the machines allow U.S. companies to compete with the low wage and low production cost operations overseas.

![]() About the Author: Chris Kuehl is the managing director of Armada and an economic analyst for IHEA. Over the last 21 years, Chris has worked with many private clients and professional associates. He writes a bi-weekly publication for Fabrinomics on the impact of economic trends for manufacturers. Among other advanced degrees, Chris has a doctorate in Political Economics and is a well-known keynote speaker, giving nearly 100 presentations a year.

About the Author: Chris Kuehl is the managing director of Armada and an economic analyst for IHEA. Over the last 21 years, Chris has worked with many private clients and professional associates. He writes a bi-weekly publication for Fabrinomics on the impact of economic trends for manufacturers. Among other advanced degrees, Chris has a doctorate in Political Economics and is a well-known keynote speaker, giving nearly 100 presentations a year.

Find heat treating products and services when you search on Heat Treat Buyers Guide.com

Find heat treating products and services when you search on Heat Treat Buyers Guide.com

What Are the Real Threats to the Economy? Read More »