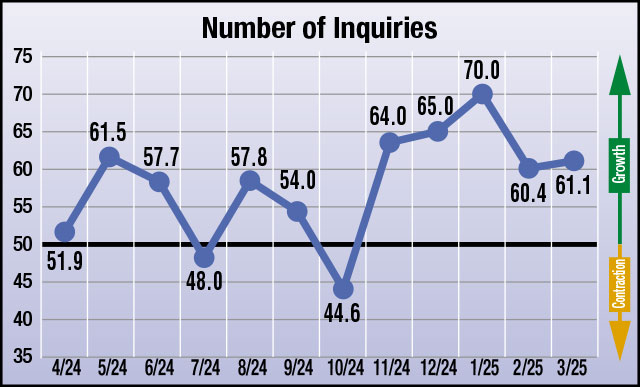

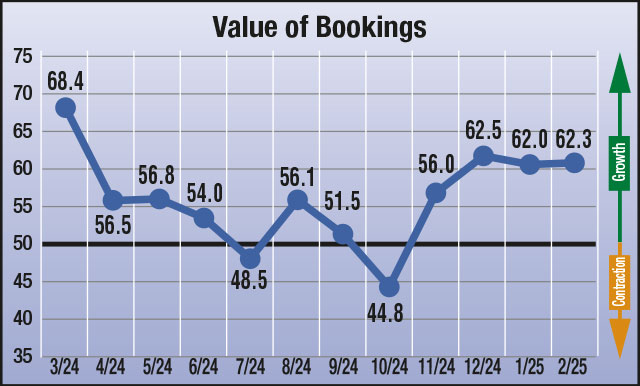

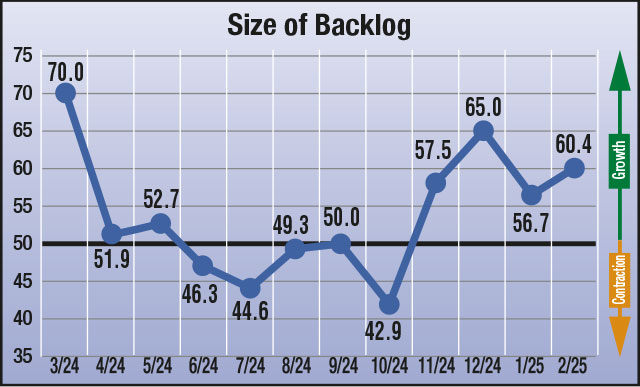

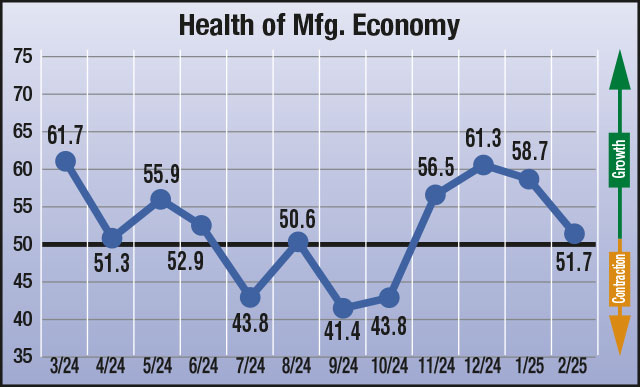

The four heat treat industry-specific economic indicators have been gathered by Heat Treat Today each month since June 2023. As the northern hemisphere looks to warmer weather, a positive outlook is reflected in three of the four economic indicators compiled in the first week of March.

Heat treat industry suppliers anticipate the economy in March to experience growth in number of inquiries, value of bookings, and size of backlog, however there is a net decrease compared to February. This is particularly shown in the economic indicators where suppliers to the North American heat treat industry expect no change over previous months in health of the manufacturing economy.

The results from this month’s survey (March) are as follows; numbers above 50 indicate growth, numbers below 50 indicate contraction, and the number 50 indicates no change:

Anticipated change in Number of Inquiries from February to March: 61.1

Anticipated change in Value of Bookings from February to March: 58.8

Anticipated change in Size of Backlog from February to March: 59.5

Anticipated change in Health of the Manufacturing Economy from February to March: 50.0

Data for March 2025

The four index numbers are reported monthly by Heat Treat Today and made available on the website.

Heat TreatToday’sEconomic Indicatorsmeasure and report on four heat treat industry indices. Each month, approximately 800 individuals who classify themselves as suppliers to the North American heat treat industry receive the survey. Above are the results. Data started being collected in June 2023. If you would like to participate in the monthly survey, please click here to subscribe.

The four heat treat industry-specific economic indicators have been gathered by Heat Treat Today each month since June 2023. Although all four economic indicators compiled in the first week of February reflect anticipated growth, there is a net decrease compared to January, as the industry adjusts to geopolitical transitions and a rebounding market.

The indicators show that heat treat industry suppliers anticipate the economy to experience growth throughout the month of February across all indices. The numbers in all four categories remain above 50 for the fourth month in a row, however, suppliers to the North American heat treat industry show cautious expectations for economic growth over previous months in number of inquiries and health of the manufacturing economy. In the latter category, respondents anticipate growth at a rate 8 to 10 points lower than the other indices.

The results from this month’s survey (February) are as follows; numbers above 50 indicate growth, numbers below 50 indicate contraction, and the number 50 indicates no change:

Anticipated change in Number of Inquiries from January to February: 60.4

Anticipated change in Value of Bookings from January to February: 62.3

Anticipated change in Size of Backlog from January to February: 60.4

Anticipated change in Health of the Manufacturing Economy from January to February: 51.7

Data for February 2025

The four index numbers are reported monthly by Heat Treat Today and made available on the website.

Heat TreatToday’sEconomic Indicatorsmeasure and report on four heat treat industry indices. Each month, approximately 800 individuals who classify themselves as suppliers to the North American heat treat industry receive the survey. Above are the results. Data started being collected in June 2023. If you would like to participate in the monthly survey, please click here to subscribe.

The four heat treat industry-specific economic indicators have been gathered by Heat Treat Today each month since June 2023. For the second month in a row, all four economic indicators reflect anticipated growth.

The indicators, which were compiled in the first week of December, show that suppliers expect the economy to experience growth throughout the month of December across all indices. This is the first month since March 2024 that the numbers in all four categories rose above 60, anticipating wide-scale improvements across the entire North American heat treat economy. In particular, the numbers increased by 6.5 and 7.5 points in the value of bookings and the size of backlog, respectively.

The results from this month’s survey (December) are as follows; numbers above 50 indicate growth, numbers below 50 indicate contraction, and the number 50 indicates no change:

Anticipated change in Number of Inquiries from November to December: 65.0

Anticipated change in Value of Bookings from November to December: 62.5

Anticipated change in Size of Backlog from November to December: 65.0

Anticipated change in Health of the Manufacturing Economy from November to December: 61.3

Data for December 2024

The four index numbers are reported monthly by Heat Treat Today and made available on the website.

Heat TreatToday’sEconomic Indicatorsmeasure and report on four heat treat industry indices. Each month, approximately 800 individuals who classify themselves as suppliers to the North American heat treat industry receive the survey. Above are the results. Data started being collected in June 2023. If you would like to participate in the monthly survey, please click here to subscribe.

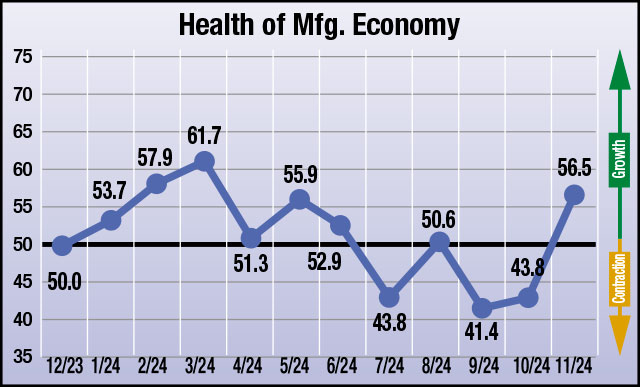

The four heat treat industry-specific economic indicators have been gathered by Heat Treat Today each month since June 2023. Last month, suppliers expected the economy to experience contraction in all four indices. This month, for the first time since May 2024, all four economic indicators are reflecting anticipated growth.

The numbers, which were compiled in the first week of November, show that responding parties expect the economy to experience growth in all four indices. In three of the four, the numbers change by more than 12 points over the past month from contraction to growth. For number of inquiries, the results from the polling increase by over 19 points, and on the other end of the indices, suppliers anticipate growth in the health of the manufacturing economy by 9 points.

The results from this month’s survey (November) are as follows; numbers above 50 indicate growth, numbers below 50 indicate contraction, and the number 50 indicates no change:

Anticipated change in Number of Inquiries from October to November: 64.0

Anticipated change in Value of Bookings from October to November: 56.0

Anticipated change in Size of Backlog from October to November: 57.5

Anticipated change in Health of the Manufacturing Economy from October to November: 56.5

Data for November 2024

The four index numbers are reported monthly by Heat Treat Today and made available on the website.

Heat TreatToday’sEconomic Indicatorsmeasure and report on four heat treat industry indices. Each month, approximately 800 individuals who classify themselves as suppliers to the North American heat treat industry receive the survey. Above are the results. Data started being collected in June 2023. If you would like to participate in the monthly survey, please click here to subscribe.

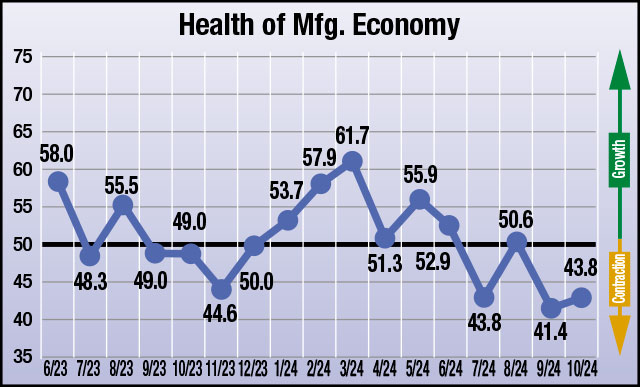

The four heat treat industry-specific economic indicators have been gathered by Heat Treat Today each month since June 2023. Last month, suppliers were split between anticipated growth and no change or contraction. This month, the four economic indicators are all reflecting anticipated contraction.

The numbers, which were compiled in the first week of October, show that responding parties expect the economy to experience contraction in all the four indices. In three of the four, the numbers change by more than 5 points from growth or no change to contraction. For anticipated health of the manufacturing economy, suppliers anticipate contraction, although in an improved range.

The results from this month’s survey (October) are as follows; numbers above 50 indicate growth, numbers below 50 indicate contraction, and the number 50 indicates no change:

Anticipated change in Number of Inquiries from September to October: 44.6

Anticipated change in Value of Bookings from September to October: 44.8

Anticipated change in Size of Backlog from September to October: 42.9

Anticipated change in Health of the Manufacturing Economy from September to October: 43.8

Data for October 2024

The four index numbers are reported monthly by Heat Treat Today and made available on the website.

Heat TreatToday’sEconomic Indicatorsmeasure and report on four heat treat industry indices. Each month, approximately 800 individuals who classify themselves as suppliers to the North American heat treat industry receive the survey. Above are the results. Data started being collected in June 2023. If you would like to participate in the monthly survey, please click here to subscribe.

The heat treating industry is under pressure to reduce its greenhouse gas emissions (GHGE), and the response has been a noble effort to attain sustainability. In two previous articles in this continuing series, guest columnist Michael Mouilleseaux, general manager at Erie Steel, Ltd., discussed the U.S. Department of Energy’s initiative related to the decarbonization of industry and its potential impact on the heat treating industry.

The endeavor to reduce greenhouse gas emissions (GHGE), albeit noble in intent, begs the question: Why is the heat treating industry being asked to reduce its greenhouse gas emissions?

Some background:

The United States’ GHGE account for approximately 14% of the total worldwide emissions.

According to the U.S. DOE, U.S. industry accounts for approximately 23% of the total U.S. GHGE.

According to the U.S. DOE, “process heating” accounts for approximately 43% of the total GHGE generated by U.S. industry.

According to the U.S. DOE, heat treating accounts for approximately 2.8% of the GHGE they have attributed to process heating.

In sum, heat treating accounts for 0.3% of the total U.S. GHGE (23% x 43% x 2.8%), and 0.04% of the worldwide GHGE (14% x 23% x 43% x 2.8%).

Why is the Department of Energy imposing natural gas restrictions on an industry that they have calculated to be responsible for 0.3% of the country’s total emissions?

Second, this administration has spent something between several hundred billion and a trillion U.S. dollars to incentivize power, transportation, and industrial sectors in their effort to stem global warming. Years from now, we will look back at this as one of the greatest capital reallocations in our history. If we can accept that the “past is a prologue,” we have a storied history of government failures to determine the future of the agricultural, aircraft, and financial sectors. This is already happening in Western Europe: Power is substantially more expensive, and industrial output has dropped nearly 6% for the past two years — the European Investment bank attributes the reduction in industrial output to “elevated energy costs.”

Perhaps it’s time for us to take notice and slow down this effort until such a time that we have the technology in place to accomplish decarbonization without eviscerating our industrial, transportation, and power industries. A greatly overused term today is “existential threat” — but our livelihood, our national security, and our way of life are, in fact, on the line.

Attend the SUMMIT to find out more about the DOE’s actions for the heat treat industry.

On www.heattreattoday.com/factsheetDOE, you can utilize the one-page resource to let governmental officials know what our industry is, who we are, who we employ, and the effect this effort has in regulating us out of business.

I want to thank Surface Combustion, Gasbarre, and Super Systems Inc. for the guidance they provided me with in navigating the technology of this subject matter.

Any errors contained herein are mine and mine alone.

About the Author:

Michael Mouilleseaux General Manager at Erie Steel, Ltd. Sourced from the author

Michael Mouilleseaux is general manager at Erie Steel, Ltd. He has been at Erie Steel in Toledo, OH since 2006 with previous metallurgical experience at New Process Gear in Syracuse, NY, and as the director of Technology in Marketing at FPM Heat Treating LLC in Elk Grove, IL. Michael attended the stakeholder meetings at the May 2023 symposium hosted by the U.S. DOE’s Office of Energy Efficiency & Renewable Energy.

Is the sky falling? Are we all doomed? Are we on the cusp of stagflation or hyper-inflation? Is this the beginning of the worst recession since the 1930s? The short answer is no.

Chris Kuehl, PhD, managing director of Armada and economic analyst at Industrial Heating Equipment Association, explains why the future may not be all doom and gloom. Read on to discover a positive outlook on the economy in this original content piece, originally published intheJune 2022 Heat TreatBuyers Guide print edition.

Chris Kuehl Managing Director, Armada, Economic Analyst, IHEA

The frothy coverage of the economy has been an exercise in extremes and one has to wonder why. Especially when we look at the actual data. The signals that are being sent are not all that dire. This is not to say that there are no problems to be aware of and there are most definitely some impending threats, but the near hysteria that shows up almost hourly is not justified by the facts — at least not as they are emerging right now. Why do some economists present these extremely pessimistic assessments and assert that a major catastrophe lies ahead?

The truth is that economists are not all that good at forecasting and predicting despite the fact this is supposed to be our job. The reality is that we have predicted 13 of the last three recessions. The comparisons between an economist and a meteorologist are not flattering but both professions have the same challenge. The data changes and it changes fast. The real purpose of the dire economic forecast is to warn. It is essentially pointing out that the economy is headed for a brick wall unless something changes. The prediction of a major recession in 2030 or 2035 or 2050 is nothing more than a call to action. If the issues that are affecting the economy are not dealt with, the likely outcome will indeed be the recession or other economic calamity that has been forecasted.

The predictions of doom and gloom are designed to call attention to major issues that demand attention sooner rather than later. All are driving the negative performance of the current economy. None of these will be easy to deal with and failure to either prepare for the impact or find a way to avert the disaster will indeed mean the economy could be headed for strains that will significantly hamper growth.

At the top of the list is the supply chain. It is safe to assume that the old system will never return. The breakdown in globalization has been due to everything from geopolitical tension to the desire on the part of companies to have better control of their processes. It is estimated that there will be a trillion dollars of reshoring in the U.S. this year alone. Nearly 70% of those doing business in China want to shift significant production to the U.S. or at least to North America. Robotics and technology allow companies in the U.S. and Europe to compete with those low production cost platforms in other countries. Despite these moves, China and other nations provide trillions of dollars of goods to the U.S. and the rest of the world which means that the reshoring effort will not eliminate the importation of material from China and elsewhere, but the dependence that has developed on the Chinese export sector will diminish. Along with the effort to bring production back to the U.S., there will be diversification when it comes to these overseas sources. There will be expansion to other Asian states such as Vietnam, Thailand, and Malaysia and there will be efforts to expand to more Latin markets such as Colombia and Brazil. Even states in Africa such as Nigeria, South Africa, Ghana, and Kenya will see efforts to expand. It is important to note that all these nations provide opportunities but also challenges.

The next challenge is connected to both the labor issue and the supply chain. Companies that struggle to find the people they want to hire will turn increasingly to automation and robotics. This has already occurred in the manufacturing sector as machines have largely replaced the people who once worked on the line in the factories. Now the automation revolution has reached the service sector with developments such as online buying, self-serve retail, and complete conversion to consumer driven interactions. The need for the labor that once dominated the service sector has largely diminished. The technology demands a higher-level worker, and those people are in even shorter supply than other skilled workers. The future is one of cobots — people interacting with and working alongside machines that have the ability to do their own problem solving. It is the robot and technology revolution that has spurred so much of the reshoring effort as the machines allow U.S. companies to compete with the low wage and low production cost operations overseas.

About the Author: Chris Kuehl is the managing director of Armada and an economic analyst for IHEA. Over the last 21 years, Chris has worked with many private clients and professional associates. He writes a bi-weekly publication for Fabrinomics on the impact of economic trends for manufacturers. Among other advanced degrees, Chris has a doctorate in Political Economics and is a well-known keynote speaker, giving nearly 100 presentations a year.

Find heat treating products and services when you search on Heat Treat Buyers Guide.com

Well, as we approach the end of November 2020 and assess the economic numbers from October, there is still no real clarity to bring a sense of understanding to our crazy year. As the Industrial Heating Equipment Association’s (IHEA)Executive Economic Summary’s October report begins, “To note that there is nothing about this year that could be considered even close to normal or predictable would be the understatement of the year, if not the decade. This was the most unanticipated and bizarre recession experienced in modern history as it was not organic in any sense. It was an imposed recession that resulted from the attempt to deal with the pandemic and all the numbers for the year have been skewed to the extreme.”

However, the reports states, “This month’s indices are far better than they were a month or so ago, but almost every one of these data points demands an explanation before we have an idea what they might be telling us about the economy.” Of the 12 indices examined, nine of them were trending positive and only three were heading downward. Interestingly, though, “that only tells part of the story.”

The rebound in demand for factory orders has been a bit more consistent than the demand for durable goods and this reflects some shifts in consumer demand. It has been pointed out that consumers have been shifting their purchasing from services to goods and that has been reflected in a variety of ways.

For example, take the data for housing starts. The summary states, “The index showed a decline, but the news has been full of very positive reports on the state of the housing sector. The index shows both the data on single family homes as well as the multi-family unit and there has been a reduction in interest in the apartment option of late.” Additionally, the demand for both single-family and existing homes has been very robust.

The auto sector has also seen interesting movement. RV sales have “never been stronger and the demand for larger vehicles has been strong as people intend to travel in them.”

“There have been several trends emerging over the last few months and the data in these indices reflect them.” The report continues, “The most obvious and expected has been the shift in consumer interest from service spending to buying goods.” Those sectors that have benefitted the most from the shift have been manufacturers, transportation companies, and importers. “The bulk of these purchases have been online and that has spurred dramatic growth in the parcel delivery sector.”

While the U.S. still doesn’t compete effectively in the production of consumer goods, “there has been an increase in demand for the sophisticated machines the US produces – especially in the realm of robotics and technology.”

Companies are turning to technology and robotics at a faster pace than ever and that boosts machine sales.

In conclusion, the reports shares, “The early indicators as far as the economy is concerned continue to be transportation and the credit environment and, in both cases, there is renewed confidence regarding the future. The unfavorable numbers (such as bankruptcy and collections and disputes) have stabilized.”

Check out the full report to see specific index growth and analysis which is available to IHEA member companies. For membership information, and a full copy of the 12-page report, contact Anne Goyer, executive director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

The latest Industrial Heating Equipment Association’s (IHEA) Executive Economic Summary begins, “The lockdown recession has been with us for over three months now, and there are few that have not experienced the impact.” How true are those words. But, be encouraged, “By most accounts this will be the bottom, and future reports will start to show slow improvement . . . there have been consistent assertions that economic growth will rebound by the third and fourth quarter.” Some may doubt the optimism, however, “there are some indications that such a forecast may be realistic.”

The indices share a consistent theme in that all show a decline “that are nearly a straight line down.” Yet, there is one notable exception: the data for the Credit Managers’ Index reveals the same severe decline, but with an upward trend at the end. The summary explains, “The index is divided into favorable and unfavorable categories from the perspective of a credit manager. The favorables include categories such as ‘sales,’ ‘applications for credit,’ ‘dollar collections’ and ‘amount of credit extended’. The unfavorables include ‘rejections of credit applications,’ ‘accounts out for collection,’ ‘disputes,’ ‘slow pays’ and ‘bankruptcies’.”

The decline that was evident in March and April was due “almost entirely to the collapse in the favorable data.” But in May, they improved substantially. Interestingly and optimistically, “Credit managers tend to think in the future as they are most concerned with what shape a debtor will be in when they are due to pay. If a company has 90 or 120 or 180 days to pay the credit manager is not going to worry about them until that time. The fact that they are getting a bit more confident now indicates that they are starting to see some positive developments down the road and not all that far away.”

The upward trend in the Credit Movement shows positive progression down the road in the not too distant future.

The other indices share a woeful tale with record setting declines. The report explains, “There is no mystery at all as to why this is the case as the lockdown was universal and sudden. There was no time at all for business or the consumer to prepare, and there have been very few options available since the declaration.” However, the U.S. Labor Department released the latest job numbers and there were expectations that the unemployment number would hit 20%, but in reality the number was 13.4%.

So, where does the economy go from here? The summary cites three factors that will come into play: First, the attitude of the consumer — “If there is to be a real rebound the consumer will have to want to resume their old behaviors and soon.” Second, the action of the government — “[This] has varied from state to state. Some have been eager to reopen and others have put off this resumption until into 2021.” Third, the course of the viral infection — this will drive the first two factors.

Buckle up, folks, the wild adventure continues!

The report is available to IHEA member companies. For membership information, and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

“It is the time to dare and endure.” Winston Churchill made that statement in 1940, and it is apropos today, as hopefully, many of us are coming to the end of the “stay at home” quarantine and will soon be free to roam again. It has also been said that it is during particularly difficult times where possibilities are mined and take flight. We will need those encouraging words in the days, months, and perhaps years ahead as evidenced in the latest Industrial Heating Equipment Association’s (IHEA) Executive Economic Summary. The report states, “This may well be the most distressing assessment of the U.S. (and global economy) since the recession of 2008. None of the bad news that follows will come as any surprise to anyone as we are all quite aware of the damage that has been caused by the reaction to the COVID 19 pandemic.”

The report explains the difference between the 2008-09 recession and that of 2020 – the current recession is an artificial one created by the forced shutdown of the economy. The U.S. enjoyed a robust economy and healthy job numbers at the beginning of the year. “The potential silver lining to all of this is that government … can reverse the process. The day that lockdowns are declared at an end, there will be recovery. Consumers will consume again, employers will hire again, producers will produce again. How much and how fast will be the prime questions.”

In the meantime, however, “Of the twelve indicators followed in this index, there are only four that are still trending in a positive direction and they will not be holding that distinction for long.” The durable goods numbers and factory orders numbers rose a little, but this only indicates there has been a delay in terms of industry response. The activity in the durable goods category is a lagging indicator. There has not yet been enough time for the reduction in activity to manifest in the numbers, i.e., airlines, heavy construction equipment, oil field machinery, farm equipment which have all taken major hits in decline.

Durable goods tracked a bit higher this month, however, be aware that its activity is a lagging indicator.

The summary continues, “The improvement in the transportation numbers may be a bit more realistic. There has been high demand in the parcel sector as everybody has been ordering things delivered.” The other sectors in transportation have not fared as well like ocean cargo, air freight, and the rail sector.

The transportation sector is showing some positive development.

The only other area that experienced a gain was in capacity utilization, “but that will shift as there is now considerably more slack in the system than was the case earlier.” Normally these numbers would reflect the pushes and pulls of supply and demand, but that process has been interrupted … and now almost every business has an overcapacity concern.

We are all living in a “waiting” mode anticipating the “all clear” proclamation. Then, as the summary report concludes, “Once some measure of control is achieved, the economy will be restarted, and then the focus will be on the speed of recovery.”

The report is available to IHEA member companies. For membership information and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.