IHEA Monthly Economic Report: Remarkable Recovery- Consumers Remain Cautiously Optimistic

Growth takes time, but celebrating the small steps and progress is good for the heart and soul– of people and country. “There has been a remarkable level of economic turnaround taking place in the last couple of months. Of the eleven indicators we watch there has been a recovery in every one of them,” so begins August’s Industrial Heating Equipment Association’s (IHEA) Executive Economic Summary.

Yes, the gains have come off record losses and numbers haven’t climbed back to where they were at the beginning of the year, however, as the report conveys, “Given the data that was showing up just a few months ago, the situation now could be far worse at this point and if there is a continuation of these recent trends there could be a recovery of that first quarter momentum by the beginning of the fourth quarter.

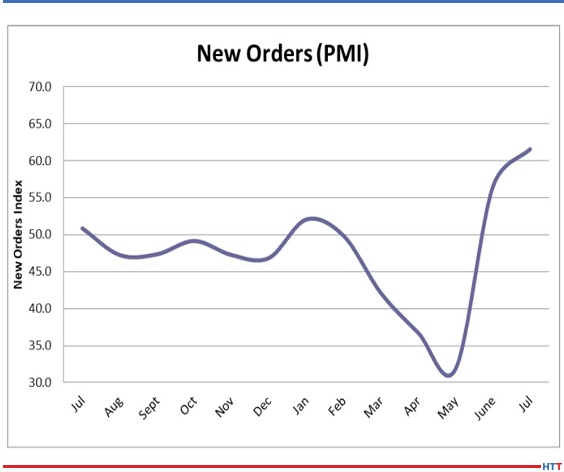

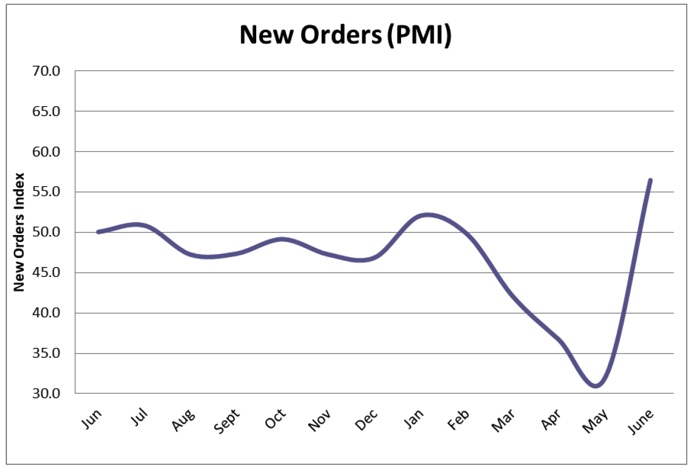

The report asks this question: With every index reading trending positive there is not much to contrast so the key issue is why. What is the prime motivation for the comeback and where might the weak points be?” Three factors are suggested for the gains. The first is the elements of the lockdown have been lifted. “Where there has been a relaxation of the restrictions, there has been economic growth.” The second reason for the economic growth is a resumption of consumer demand. “It was hoped that consumers would be eager to resume their old habits but there was no guarantee, and there was some hesitation as far as consumption was concerned. That largely vanished by the middle of the summer.” The third growth factor was the producers’ willingness to meet the recovering demand. “Production levels have been increasing through the last few months and there has been little indication that activity was being slowed deliberately as a means by which to boost prices through manufactured shortages.”

What is a potential weak area that could adversely affect the economy? The short answer– the election. “Perhaps the most potent unknown surrounds the election. There is always a concern when the possibility exists for a change in leadership. That concern ramps up when there is more at stake than just the White House. The business community is affected more by [who] holds power in Congress as this is where those fiscal decisions are made.

To highlight just two indices, first, take a look at the New Home Starts where the housing market “is booming in almost every respect. The analysis states, “The surge has been seen primarily in the single-family home category as there has been an exodus of people from urban areas to the suburbs and exurbs.” Why? Because due to the lockdown restrictions, people are tired of cramped living conditions, and many are craving more space in the suburbs. “The majority of the factors that stimulate home buying are trending in a positive direction. Mortgage rates remain at very low levels and lenders are still willing to do these home loans.”

The second index that highlights a viable and healthy rebound is the Factory Order index. “The gearing up for the holiday season is well underway as the retailers have clearly signaled that they are expecting a very early buying season. They will be entering the period with an ‘inventory light’ strategy and will be turning the entire month into ‘Blackvember’ with early sales and discounts designed to capture the attention of the early shopper.”

Resilient has often described Americans throughout our history, and this period in time is no different. Challenges make us stronger, and hopefully, wiser. Here’s looking to a continued growing economy and wisdom in decision-making.

Check out the full report to see specific index growth and analysis which is available to IHEA member companies. For membership information, and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.