Automotive sales have been stable, which means the whole sector has been stable (Click image to enlarge)

February’s Industrial Heating Equipment Association’s (IHEA) Executive Economic Summary suggests, “The numbers revealed in this month’s index will someday be remembered as the ‘good old days.’ This will be the last version that can be termed “PCV” or pre-corona virus.” The report continues, “It will be important to look back on the last couple of months and remember that conditions looked pretty decent at the start of the year.”

The three indices that are trending positive include new automobile and light truck sales which reveal strongly that consumers favor their new vehicles. There was also a nice boost in steel consumption which suggests that there has been more construction activity in the public sector. Additionally, despite the threat, consumers remained active as factory orders were also up slightly.

While eight indices are trending downward, the summary reports, “The semi-good news is that several of the negative readings are only slight in that category.” The biggest declines were seen in “metal prices (and commodities in general) as well as capital expenditure, credit and transportation. The only one that really crashed hard was capital expenditure and that is partly due to the slump in manufacturing that started last year.”

The capacity utilization dip still registers in the high 70s (Click image to enlarge)

A little less dramatic in declines are the housing market, which still remains healthy although new home starts are down; and, capacity utilization, that has been sinking, but “is still not all that far off the pace considered normal.” The durable goods numbers and the data from the Purchasing Managers’ Index also slowed down, but not significantly.

“The next month will show drastic reductions in business activity in many sectors and the job losses will start to mount. The hope on the horizon is that COVID-19 behaves like others of its kind and starts to fade as the weather warms. If the worst of the impact is in March and April the recovery will be obvious by June and July.” states the report.

It is an uncertain time for everyone, and we can all resonate with this concluding thought, “It is hard to say what these numbers tell us. This is uncharted territory for the US.”

The report is available to IHEA member companies. For membership information and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

On February 27th, Heat Treat Todayconducted an initial Coronavirus Impact Study. We wrote about the findings on March 4th. Click here to see that initial report. Considering the historical uniqueness of what is happening and the impact that the virus and, more importantly, the impact of the reaction that has been mandated by federal, state, and local governments, Heat Treat Today decided to conduct a slightly expanded follow up study (Phase II) on March 20th — roughly 3 weeks after the initial study. Below is an analysis of the results of Phase II and where possible a comparison between Phase I and Phase II results.

Publishers Note: The coronavirus/COVID-19 situation has been accompanied by media coverage that some describe as sensational and panic-creating. Heat Treat Today’s desire is to objectively report impacts without commentary and without increasing panic.

The Phase I (February 27th) survey netted more respondents, 113, than the Phase II (March 20) survey, 75. The decrease in responses may be attributed to the day of the week that the survey was deployed — Thursday for Phase I and Friday (late afternoon) for Phase II. The length of the survey may have also impacted the response rate — Phase II having several more questions than Phase I. Neither study has enough responses to be considered “scientific” and Heat TreatToday strongly recommends that no important decisions be made based on the results of these studies.

Additionally, the phrase “coronavirus” was used extensively in Phase I whereas “COVID-19” was used extensively and in place of “coronavirus” in Phase II. It is understood that these terms are different and stand for different things. For the non-medical professional, we assumed that these two terms will mean essentially the same thing and they were used interchangeably. Our apologies to medical professionals and other who know the difference.

Finally, this survey was sent to roughly 700 heat treat industry SUPPLIERS, not end-users. The desire was to see what impact the virus and the subsequent response of governments and businesses was having on the heat treat industry specifically, and not on the wider industrial economy as a whole.

Current Impact

Q: Has the coronavirus/COVID-19 ALREADY impacted your business?

The two studies were divided up into two broad sections: 1) what impact the virus has ALREADY had, and 2) what impact the virus is ANTICIPATED to have.

The percentage of respondents claiming that COVID-19 had already impacted their business essentially doubled from Phase I to Phase II going from roughly 40% to nearly 80%. And the number of respondents saying that there has been no impact fell from nearly half in Phase I to roughly 12% in Phase II. Below, Phase I results are shown first, then Phase II results.

Phase I (click to enlarge)Phase II (click to enlarge)

Q: How has the coronavirus/COVID-19 ALREADY impacted your business?

The responses here were also significantly different. Please note that the charts below are not 100% comparable. While both green bars denote supply chain difficulties and both blue bars represent travel restrictions, there was a third option added to the Phase II options that was not in Phase I. Therefore, the tan or yellow bar actually represents two different answers between the studies as does the blue bar at the bottom. Please read these charts and the tables that follow them carefully to see the difference between the last two bars.

Suffice it to say, however, that while supply chain concerns did not increase significantly between the two studies, travel restrictions nearly tripled going from 30% in Phase I to nearly 90% in Phase II. Effectively, travel is banned in the North American heat treat industry … something never before experienced.

One final point. In the Phase II chart below, you’ll notice that the last option is “Other (please specify).” For the sake of relative brevity (!), these “Other” comments have not been included in this report. If you’d like to see these comments, please email htt@heattreattoday.com and request a full “Phase II Coronavirus Report.”

Phase I (click to enlarge)Phase II (click to enlarge)

Q: What steps are you ALREADY taking to minimize the impact?

In Phase II, an additional question was asked regarding what steps have already been taken to minimize the impact of the virus. There was no equivalent question in Phase I. Below are the results. Please notice that the complete wording of the answers are shown in the table below the chart and the “Other (please specify)” answers are not shown, but may be obtained by emailing htt@heattreattoday.com.

Phase II (click to enlarge)

Anticipated Future Impact

In both studies, we then moved from the CURRENT situation to what people were ANTICIPATING for the future.

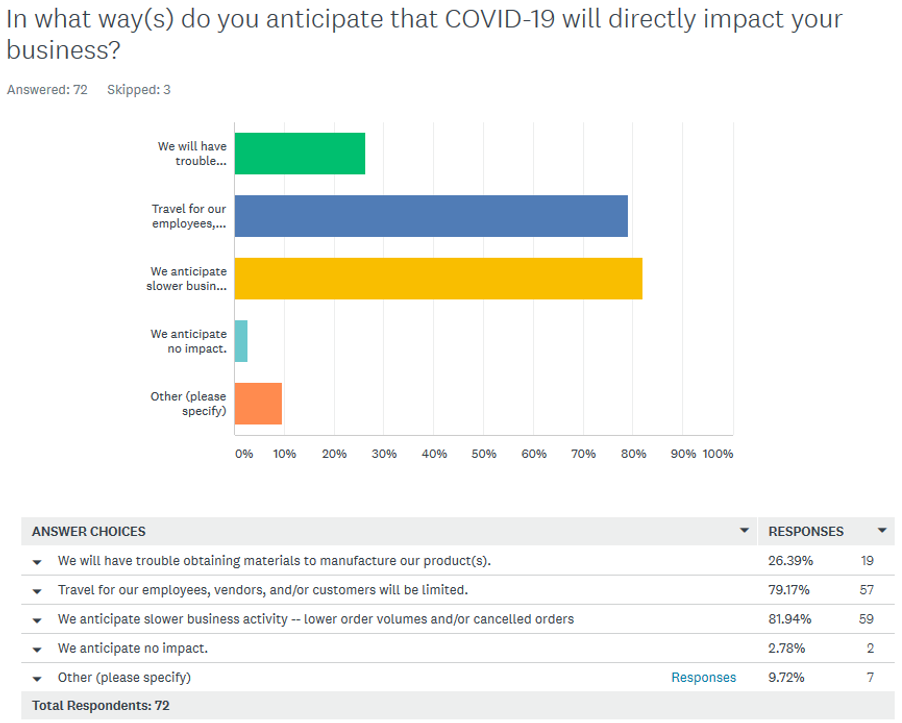

Q: In what ways to you anticipate that the coronavirus/COVID-19 will impact your business?

The top bar, the green one, represents an anticipated difficulty with a company’s supply chain — difficulty getting materials to manufacture their heat treat product or component. This number stayed at roughly 25% in both studies.

The green bar is also the same in both studies representing travel restrictions. This number, however, took a huge jump between Phase I and Phase II — 43% to 79%.

There was an additional answer added to the Phase II study so the tan/yellow bar represents two different things in the charts below. In Phase I, the yellow bar represented “Other” responses. In Phase II, it represents an anticipated drop off in business levels and it was this answer that gleaned the highest number of responses — just over 8 of 10 respondents anticipated a drop in business levels due to the virus.

Phase II (click to enlarge)Phase II (click to enlarge)

Q: What steps do you anticipate taking to minimize the impact of the coronavirus/COVID-19?

There was another additional question added to the Phase II study asking what actions the company anticipated taking to reduce the impact of the virus. Below are the responses.

Phase II (click to enlarge)

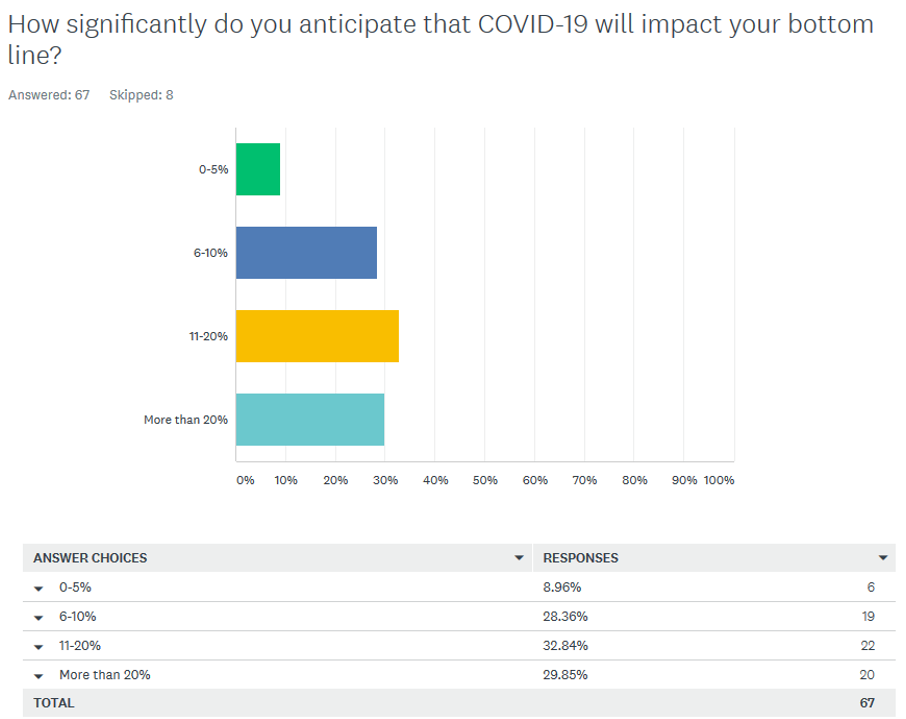

Q: What impact will the coronavirus/COVID-19 have on your company’s bottom line?

On this question, it is safe to say that the answers were significantly less optimistic in Phase II than they were in Phase I. In Phase I, over 50% felt that the virus would impact their bottom line 5% or less. In Phase II, the “5% or less” answer was given less than 10% of the time, meaning that over 90% of the respondents anticipate that the virus will have a greater than 5% impact on their bottom line. In fact, the highest number of respondents chose “11-20%,” and the second largest group was the group anticipating “Over 20%”.

Phase I (click to enlarge)Phase II (click to enlarge)

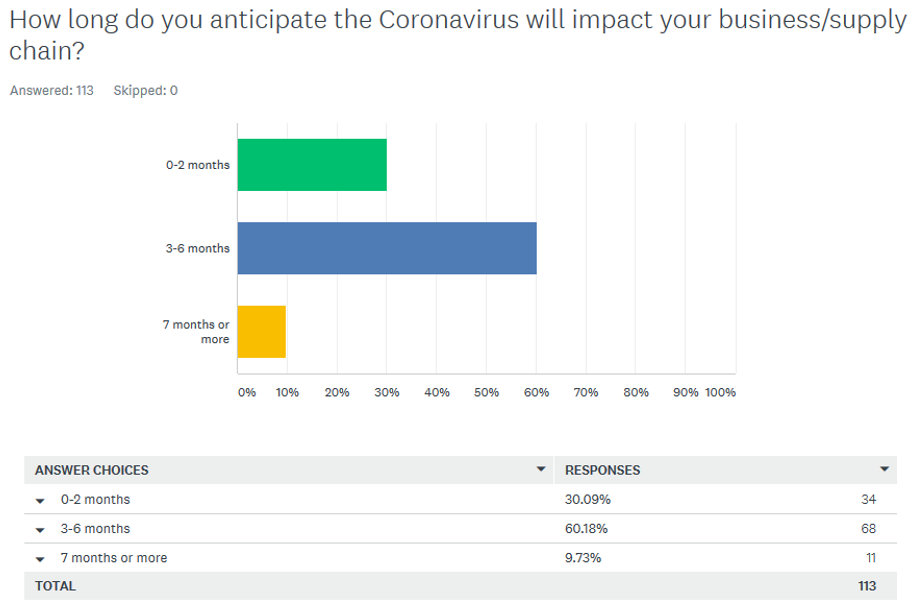

Q: How long do you anticipate the coronavirus/COVID-19 will impact your business?

This is another question where the answers were significantly different between the two studies. The “3 to 6 month” answer came in nearly identical on both studies sitting at roughly 60% in both cases. Marked changes occurred, however, on both sides of the “3 to 6 month” answer. Those anticipating an impact of “0-2 months” fell by nearly half from roughly 30% in Phase I to just over 17% in Phase II. The big gainer was in the “7 months or more” category where the numbers over doubled from only 10% in Phase I to 25% in Phase II. Obviously, the heat treat industry is bracing for a much longer impact than initially anticipated in Phase I.

Phase I (click to enlarge)Phase II (click to enlarge)

Actual Sickness

The above question was the LAST question asked in the Phase I study. Phase II respondents were given the optional opportunity to answer one more personal question. The reason for asking this question was to get at the actual health impact of the coronavirus/COVID-19 verses the impact caused by the reaction of governments, media, and others who might be unduly heightening anxiety levels whether purposefully or unwittingly. As you can see from the chart and table below, nearly 80% of the respondents chose to proceed with the optional question.

Phase II (click to enlarge)

The question itself is rather long and can be read in the chart below. As you can see, of those proceeding to this more personal question, over 80% chose to actually answer the question. Of those answering the question, nearly 95% knew of no one in the heat treat industry (as defined by the question) currently infected with the coronavirus/COVID-19 and a full 97% knew of zero or one person infected. (Please note that the percentages above are based on a base of 38 people who chose to give a numeric answer.)

Phase II (click to enlarge)

A Complete Copy of the Report with “Other” Comments

If you’d like to see a complete copy of the Phase II results (with all personally-identifiable or company-identifiable information removed), please email htt@heattreattoday.com and request a copy of “Phase II Coronavirus Report.”

“Optimism” may be a good description to highlight January’s Industrial Heating Equipment Association’s (IHEA) Executive Economic Summary. It states, “The US economy has started the year in better shape than had been expected. Now the attention of the economist has been focused on two questions. The first, why the headwinds that were expected to slow things down haven’t? And the second, how long can this situation be expected to last? Despite the predictions that consumers would become weary and businesses would begin layoffs at the start of 2020, “… some of the pressure was released with the ‘phase one’ deal with China and the consumer just seemed to power through their concerns.”

New home starts experienced an unexpected and encouraging rebound

The summary reports, “In looking at the index readings this month, the news is pretty good. Of the eleven, there are seven that are trending positive and four that are pointing in a more negative direction. The more important note is that the good news readings are very strong and the negative readings are not so dramatic.”

Of the seven positives indices, new housing starts experienced a dramatic rebound, and the housing sector is as strong as it has been in some time. Additionally, the reports states, “There was also some significant gain in terms of steel consumption. The automotive sector and the energy sector have helped boost demand.”

Significant growth in new orders after 5 consecutive months in decline

One other significant area of growth to note is the PMI, “There was a very impressive rebound as far as the Purchasing Managers’ Index was concerned. The overall index jumped back into expansion territory with a reading of 50.9 but an even bigger leap was noted in the New Orders index as it went from 46.8 to 52.0. Given the future orientation of the new orders data, this is good news indeed.” Other indices showing a positive growth were capital expenditures, durable goods, factory orders, and the credit manager’s index.

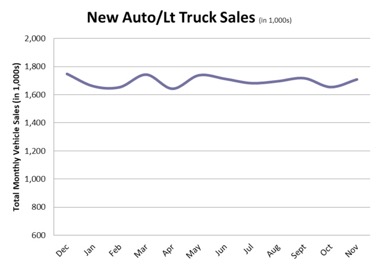

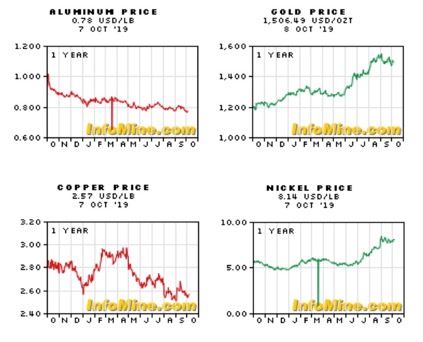

Those indices that weren’t as upward trending, but not “all that depressing” were new automobile/light truck sales, falling metal commodities prices due to lack of demand, and capacity utilization. The transportation index seems to be more of a concern, “The slip has been mostly in the rail and maritime sectors thus far as both have been affected by the trade wars and other interruptions in the global economy. The bottom line is that the bad news data has not been all that serious and most are likely to see some improvement in the future if the good news data keeps coming in.”

In conclusion, the news is better than expected this month with much growth. However, we can’t ignore the coronavirus and that its effect on the global economy has yet to play out completely.

The report is available to IHEA member companies. For membership information and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

The Hubei province of China has now been shut down for three weeks due to the Coronavirus outbreak, and industries around the world–including automotive and aerospace–face continued uncertainty about the future while an industrial powerhouse roughly the size of Sweden sits quiet. Despite more than 900 lives having been claimed by the virus in China thus far, some companies, including Tesla and Airbus, have cautiously reopened and gone back to work with the government’s blessing while others remain shut.

Airbus’ Chinese division has been given permission by Beijing to “gradually increase production, whilst implementing all required health and safety measures for Airbus employees, which remains the top priority.” Their final assembly line in Tianjin has restarted operations. In response to the Chinese government’s statement, the company stated, “[We are] constantly evaluating the situation and monitoring any potential knock-on effects to production and deliveries and will try to mitigate via alternative plans where necessary.”

Meanwhile, the automotive industry continues to be plagued by shutdowns that are starting to impact global manufacturing. Hyundai Motor, General Motors, Volkswagen, Renault, and Toyota Motor have extended their suspension of operations. Factories in the Hubei province expected to open on February 13 have had that deadline extended, and some provinces and districts have instructed companies not to reopen until March 1. The province of Hubei accounts for 9% of all Chinese automotive production.

Razat Gaurav, CEO Llamasoft

The impact of the shutdown is expected to extend beyond auto companies to manufacturers of auto parts as well. According to Razat Gaurav, CEO of Llamasoft, an AI-driven software development company that works with several automakers including Ford and General Motors, “Most OEMs single source components for new vehicles and China is a large supplier of those. Thus, there is exposed risk. The automotive industry has been going through a ‘regionalization’ trend for the last 5 to 8 years . . . Even so, there is a ripple effect in other parts of the world. For example, Hyundai is one of the first automotive companies announcing closures outside of China, at its South Korean factories; France’s Renault also announced a shutdown in its South Korea facilities. Fiat Chrysler warned it may need to halt production in one of its European plants due to a shortage of parts. While we have talked a lot about the manufacturers themselves, the impact on the supplier base is significant as well.”

“There is a good bit of optimism regarding the 2020 economy,” this month’s Industrial Heating Equipment Association’s (IHEA) Executive Economic Summary begins. “The unemployment rate is still very low and there have been several months of solid job growth. The expected growth rate for the year remains close to 2.0%.”

The five index readings that are moving in a positive direction include new automobile/light truck sales, new home starts, industrial capacity utilization, metal pricing, credit movement as measured by the Credit Managers’ Index and the Transportation Activity Index. The report continues, “The latter two readings have a history of being ‘canaries in the coal mine’ as they react quickly to changes in economic momentum and tend to point the way for the rest of the economy later.” However, the power of the consumer is key to growth as the summary states, “The common factor, as far as growth, is anticipation of a decent short-term trend and the existence of confidence within the ranks of the consumer.”

The report also conveys that with the good news, there is some concern for what to expect later in 2020. The six indices that have trended in a more negative direction include steel consumption, the new orders index from the Purchasing Managers’ Index, industrial capacity utilization, capital expenditures, durable goods and factory goods. The summary reports, “The negative activity is almost entirely focused on production decisions.”

It appears as if Americans are feeling confident as they bring in 2020, “The consumer is still in a good mood and has yet to start worrying about the possibility of layoffs or the arrival of inflation. That translates into wishing to buy cars and homes and these indicators are therefore trending up a little.” However, as the reports concludes, it is an election year and, “Election years always create uncertainty.”

The report is available to IHEA member companies. For membership information and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

In this month’s IHEA Executive Economic Summary, the indices show “the unemployment rate is very low. . . and the consumer remains in a good mood.”

Consumers show confidence as evidence of New Auto/Lt Truck Sales.

Of the eleven targeted index readings, seven are pointing in an optimistic direction. The most positive numbers are coming from new automobile/light truck sales, new home starts, steel consumption and credit movement. The report states, “The three areas that stimulate steel consumption are vehicle manufacturing, construction, and to a lesser extent, durable goods and appliances. All three of these sectors have shown some signs of growth in the last month with commercial construction leading the way.”

The other three positive indices in that category are metal prices, capital expenditures, and factory orders. The summary reports, “The rate of factory orders has tapered off a bit, but the levels have remained more or less stable.” The trade wars may spur some reactions, too. “The restrictions on trade with China has altered supply chains as other nations step up to supply, but there has also been some additional purchasing from US factories.”

The rate of factory orders has tapered off slightly, but the levels have remained stable.

The concerning news is that these three are barely moving in an upward direction. Of the four that are trending in a negative direction, capacity utilization, new orders (PMI), durable goods orders, and transportation activity, the slump is pronounced. “This is the kind of data that encourages that sense of caution and trepidation.”

As the IHEA Economic Summary reports, “There is a little something under the tree for both the optimist and the pessimist.”

The report is available to IHEA member companies. For membership information and a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

New orders turned upwards following several months of downward motion.

What impact does the coming political election have on the 2020 economy? As this month’s IHEA Executive Economic Summary reports, “Election years tend to depress consumers, business people and investors alike. The two parties try to outdo one another with tales of gloom and doom unless you vote for them and the sense is that the world is teetering on the brink.”

That being said, the report also encourages optimism when it states, “It should be noted that many of the index readings that turned negative are only slightly down and many are still higher than they have been much of the year.”

Metal prices, new orders and recorded in the PMI, capital expenditures, and the transportation index all trended upward in October. According to the report, the fact that the PMI has started to trend upward, even though it is still below 50, is a good sign for the months ahead.

Regarding capital expenditures, the report states, “The capital expenditures numbers are better than expected given the data on capacity utilization, but it seems there is still a demand for replacement equipment even if there is less demand for new equipment to support growth.”

Industrial capacity utilization continued to slide in October adding to worries about a potential recession.

With regard to the seven downward trending indices, the report states that “they are not all that bad.” Indices in this group include new automobile and light truck sales, new home starts, steel consumption, and industrial capacity utilization to name a few.

Concluding the report is the following statement, “These have not been massive drops and there is no sense of an impending crisis, but this kind of weakness doesn’t leave much wiggle room should there be a real recessionary trend. The overall sense of trepidation in the industrial sector is driving most of the current level of angst.”

Anne Goyer, Executive Director of IHEA

For a full copy of the 12-page report, contact Anne Goyer, Executive Director of the Industrial Heating Equipment Association (IHEA). Email Anne by clicking here.

Despite predictions that trade wars, oil prices, and cautious business decisions would slow economic growth, the economic readings, reported monthly by the Industrial Heating Equipment Association’s Executive Economic Summary, “show some of that caution, but many had expected a drastic reduction in activity by this point, and that has not emerged.”

Trending upward were nine areas including those with a small bump from the sales of new automobiles and light trucks. This steady rise has been reflected throughout the year, from last December’s high at 1,749 million to this month’s 1,718 million.

Over the past several months there has been a marked improvement in metal price data. The PMI New Orders that had been on a sharp decline over the past months have leveled off and are similar to last month’s reading.

Metals Pricing shows distinct improvement over last several months

The biggest jump was reflected in the new home starts with multi-family and high-end sectors driving the market; additionally, there was a bump in commercial building. Steel consumption also saw a rise due to the demand of vehicle manufacturers.

According to IHEA’s economist, if there is an overall conclusion it’s that most of the dire predictions concerning the economy have not come to fruition, however, there remains considerable unease. “The variables have been hard to determine–much less predictable.”

Anne Goyer, Executive Director of IHEA

The 12-page monthly report is comprised of an introductory summary page, and then one page each to analyze in detail eleven indices chosen specifically for their impact on the thermal processing market.

To receive a full copy of this report, contact Anne Goyer, Executive Director of IHEA

The monthly Executive Economic Summary, crafted for the member companies of the Industrial Heating Equipment Association (IHEA), showed that the global economy is slowing but there continue to be signs of potential growth as well. All in all, this month’s report was less optimistic than previous reports, but, to quote the report, “At this point, there is data to support whatever mood you choose to be in.”

Five of the eleven indices were trending upward. Among the positive trending indices were new automobile and light truck sales, steel consumption, metal prices, factory orders, and the credit managers index. All of these indices push upward.

Purchasing Managers Index continues to slide

Six of the indices went south, including the Purchasing Managers Index (PMI), capacity utilization, and durable goods. Housing and transportation also were soft.

According to IHEA’s economist, much of what we are seeing is a global slowing of the manufacturing economy. Citing concerns like Brexit and the looming trade war with China, the report indicates that much of what the global manufacturing economy is experiencing is bigger than the U.S.

The 12-page monthly report is comprised of an introductory summary page, and then one page each to analyze, in detail, eleven indices chosen specifically for their impact on the thermal processing market.

Anne Goyer, Executive Director of IHEA

To receive a copy of the report, contact Anne Goyer, Executive Director of IHEA.

Two leading industrial process fluids suppliers have merged to create a new company which will continue to service the aerospace, aluminum, automotive, machinery, industrial parts manufacturing, offshore, steel, and tube and pipe industries.

Quaker Chemical Corporation and Houghton International have combined to create Quaker Houghton (NYSE: KWR), positioning the new company to be a global leader in industrial process fluids to the primary metals and metalworking markets. Along with the new name, the company revealed a new logo and brand representing the combined companies. The company will continue to be listed on the New York Stock Exchange and trade under the “KWR” ticker symbol.

Michael F. Barry, Chairman, Chief Executive Officer, and President, Quaker Houghton

Quaker was founded in 1918 and Houghton in 1865. The combined $1.6 billion revenue company employs 4,000 associates serving 15,000 customers worldwide.

“We are rooted in companies commonly acknowledged as authorities in industrial fluids and valued experts in customer processes,” said Michael F. Barry, Chairman, Chief Executive Officer, and President of the new company, previously serving Quaker Chemical in similar capacities. “Our similar cultures and values, combined with the talent and resources we bring to Quaker Houghton, create exciting opportunities to deliver innovative solutions that will help our customers’ operations run even more efficiently and effectively.”

Specific products the company offers include metal cutting and forming fluids, corrosion protection fluids, specialty hydraulic fluids, and steel and aluminum rolling oils. In addition, legacy-Houghton customers will benefit from Quaker’s strength in specialty greases, high-pressure die casting, mining specialties, surface treatment and bio-based lubricants, while legacy-Quaker customers will now have access to Houghton’s heat treatment quenchants, offshore hydraulic fluids, metal finishing products, and a broader metal removal fluids portfolio.